If you can also call yourself the proud owner of a hyperactive dog, such as my Miniature Poodle Baloo, you’ve probably been wondering whether getting pet insurance for dogs might be worth it.

Vet bills can quickly go into the thousands of dollars. The only problem is that you never know how much medical care your dog will need during his lifetime. So, you’re pretty much left with 2 options: you either self-insure by putting a certain amount away per month. Or you get a pet insurance that can cover up to 90% of all of your vet bills, with sometimes only 1 deductible per year.

After doing some research on reddit, about 90% of dog owners who have pet insurance for their dogs highly recommend it! The majority have saved hundreds or thousands of dollars and the peace of mind is priceless!

Table of Contents

How much is pet insurance for a dog?

Now, let’s look at the question “is it worth getting pet insurance for dogs” in more detail.

First of all, how much does pet insurance for a dog actually cost?

This depends on a few different factors.

Which factors determine your dog’s insurance premium?

When you apply for your dog’s insurance, the company looks at a few different factors to determine your monthly premium. First and foremost, the insurance company may check if your dog has any pre-existing conditions before enrollment. If that’s the case, most companies will either set the premium pretty high or they simply won’t cover any illnesses related to that condition.

Then, they look at your dog’s age. Older dogs are more likely to suffer from diseases that will cause high vet bills, which is why the premium will be more expensive.

And last but not least your dog’s breed also plays an important role. Toy and small breeds are usually cheaper because they don’t cause very high bills. Large and very large breeds tend to be the most expensive because they often suffer from hip dysplasia and arthritis when they get older.

Mixed breed dogs’ premiums tend to generally be lower than premiums for pure-bred dogs because they’re less susceptible to certain breed related illnesses.

As you can see, by far the best option is to get pet insurance as soon as you bring your puppy home. This helps at getting insurance before potential pre-existing conditions and the premium will be the lowest possible.

However, keep in mind that your living location also plays a role in determining your monthly premium. If you live somewhere where vet bills are quite expensive, your premium will naturally be higher, as well.

What kind of plans do pet insurances offer?

Apart from those basic factors that concern your dog, most pet insurance companies also offer different plans.

There are normally 4 different types of plans:

- Accident-only plans: only covers costs due to injuries, such as a car accident, poisoning or ingestion of a toy etc.

- Accident and illness plans: most common plan, covers costs due to injuries and illnesses, such as allergies, cancer and digestive issues.

- Plans with embedded wellness: these plans cover the same as nr. 2. Additionally, they usually covers things such as dental care, worm, tick and flea treatment, groomer, vaccinations, check-ups and more.

- Endorsements or riders: Riders are additions to accident plans, such as cancer riders. Endorsement plans offer wellness and cancer treatment as add-ons. Some insurances also offer optional wellness plans that are separate from the insurance plans.

Related article: How far can a dog hike in a day?

How much is the monthly premium on average?

According to Valuepenguin the average monthly cost for pet insurance for dogs is $47.20 for plans that cover both accidents and illnesses. According to Healthypaws, a 2-yo mixed breed medium sized dog costs about $35/month, if you live in Denver, CO.

From my own research I found that $35/month seems to be about the average. For exact numbers, it’s best to get a quote from several insurance companies, so that you can compare them directly.

Keep in mind that the premium will most likely change, as your dog gets older. However, some insurances also offer fixed premiums.

How high is the deductible and the coverage?

From what I’ve read on reddit, the most common deductible was $250 per incident with a coverage of 90%. With most companies you can choose a deductible of $0 to $1’000 per incident, sometimes even per year. The higher the deductible, the lower the monthly premium.

For coverage the most common is between 70% and 90%. The higher the coverage, the higher the premium.

Top pick insurances for dogs

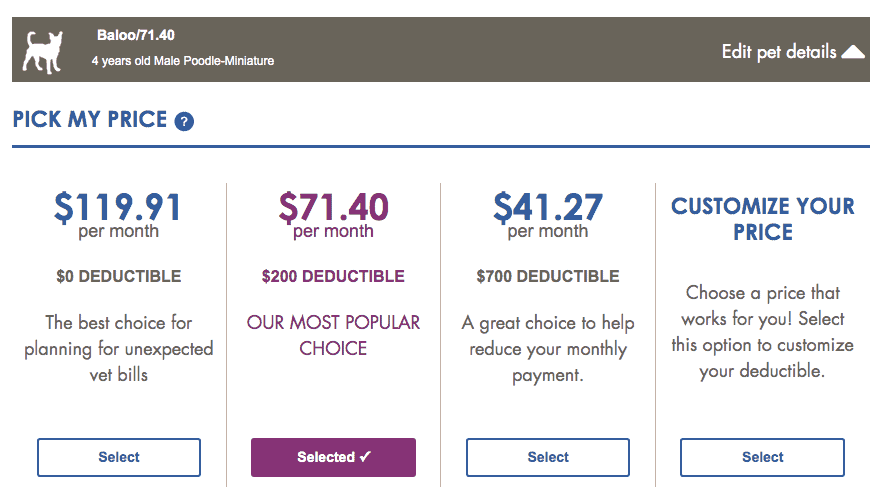

In order to get a better grasp on what plans might actually look like, I got quotes from 4 different insurance companies. I used my 4-yo Miniature Poodle Baloo as an example and set the location to Cleveland, Ohio.

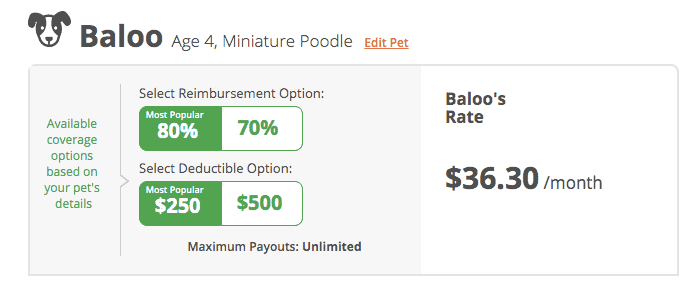

Healthy Paws

Healthy Paws gives you quite a good overview right from the start. You have 2 options to choose from regarding the reimbursement option and 2 options regarding the deductible.

According to their reimbursements examples, you can also choose a 90% reimbursement and an annual deduction of $100.

Embrace

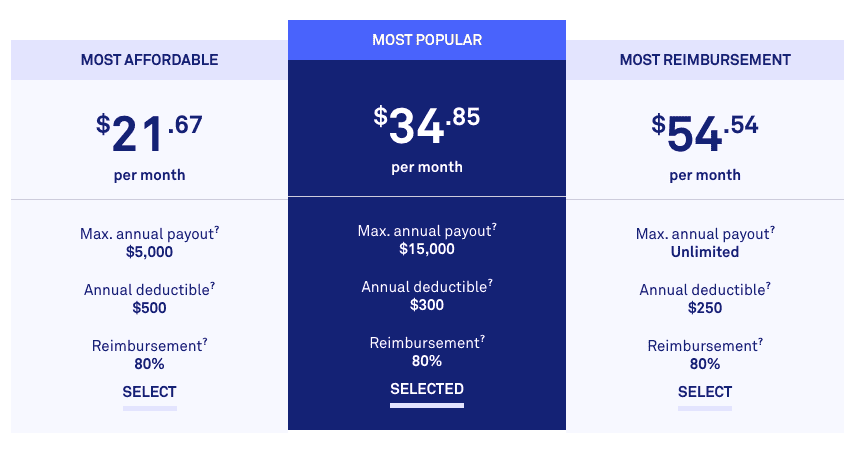

Embrace offers a lot of different options.

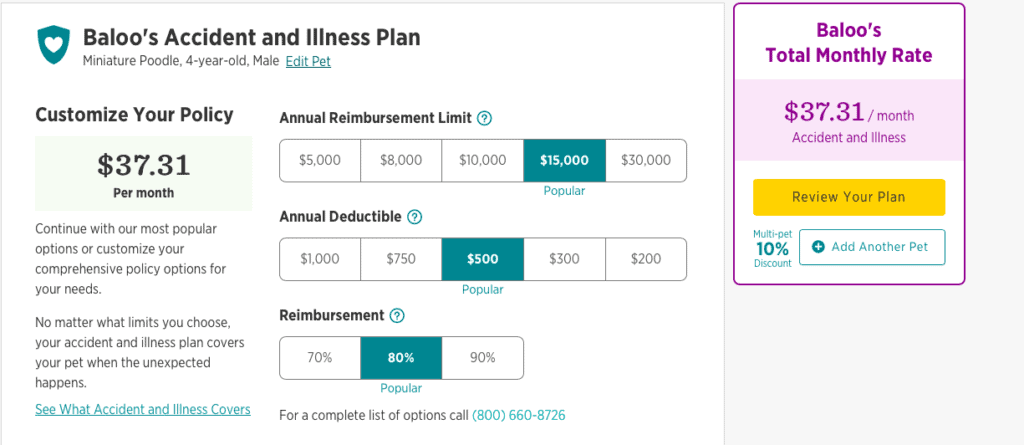

In my quote I chose the most popular plan which has an annual reimbursement limit of $15’000, an annual deductible of $500 and a reimbursement of 80%.

This would leave me with a monthly premium or $37.31 which is pretty much in line with what I read from other dog owners.

Happy Embrace customer here. The premiums are SO much lower when compared to Healthy Paws and Trupanion. I pay $38/mo for the same coverage as a $55/mo plan from the other companies.

caffeinatedlackey on reddit

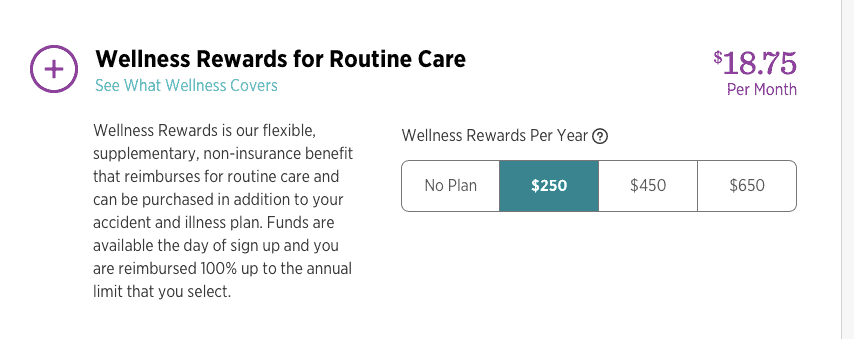

One cool thing is that you can choose an additional wellness plan where things like check-ups, tick, flea and worm treatments are included.

For a yearly wellness reward of $250, I’d pay $18.75 extra per month.

If that sounds like something you could use for your dog, get your own quote here.

PetPlan

PetPlan showed me their 3 most common options, all having a reimbursement of 80%.

From what I’ve found you also have about the same choices when it comes to reimbursements, you can even go up to 100%. And the lowest annual deductible I’ve seen was $50.

Trupanion

While Trupanion is more expensive than their competitors, they offer a lifetime deductible, which I haven’t seen anywhere else. And they also seem to be the only insurance offering direct payments to the vet, instead of reimbursements.

PetAssure – the veterinary plan as an alternative

PetAssure isn’t a pet insurance, but a veterinary plan. This means you pay a monthly premium, starting at $6.58/month and you get 25% off each vet bill. No waiting period and no exclusions. Every vet treatment is covered!

The only thing you need to do is to show your PetAssure card when you’re at the vet and you automatically get a discount of 25%.

Pretty cool, huh?

This is a great option if you just want to keep your annual vet costs low but have enough funds to cover any unexpected high bills, such as for a surgery for your dog.

Click here to learn more.

Is it worth getting pet insurance for dogs?

Now, let’s wrap this all up: is it worth getting pet insurance for dogs?

As you can see, the monthly premiums are quite reasonable if you choose a reimbursement option of 80% and a deductible of around $300.

If we take an average of $50/month (because premiums will naturally go up over time) then that sums up to $600/year. And if we calculate that over a dog’s average lifetime of 12 years, then we end up with $7’200.

Now, if your pup is super healthy and never has any major infection and doesn’t need any surgery, then it probably looks like a lot of money. However, if your pup has an accident and needs surgery or maybe develops an illness for which he needs daily medication, or he gets cancer, then vet bills can quickly rise over $10’000.

Related articles:

Nr. 1 reason: peace of mind

The main reason we get insurances is to cover huge, unexpected expenses. It’s like a safety net in case you get hit with a vet bill of several thousand dollars. This is why I think it’s best to look at pet insurance as if it was a car insurance, instead of a health insurance. You invest in security for very catastrophic events with very high costs!

But the real nr. 1 reason for pet insurance is the peace of mind!

It’s true that pet insurance will only pay off if your pup develops some serious disease, such as cancer, or has a couple of accidents over the span of his lifetime.

But the point is, you don’t know if that’s going to happen!

And do you ever want to be faced with a decision to make a potentially life-saving treatment, that costs $10’000 or having to put your dog down because you can’t afford it?

That’s probably the worst nightmare of all dog owners!

Get it as early as possible

For the examples above I used Baloo who is already 4 years old. If you get the insurance for your dog when he’s still a puppy, it’s likely going to be much cheaper. The reason for that is that puppies usually don’t have any pre-existing conditions and they usually don’t suffer from very expensive illnesses early on.

However, some puppies live quite a dangerous life! I’ve heard tons of stories of puppies eating toys, chocolate bars or jumping off a rock and breaking a leg. Puppies are rowdies and it’s not uncommon to have to visit your vet during the first few weeks of bringing your puppy home.

Self-insuring as the alternative

Now, I want to be completely honest with you: I don’t have any pet insurance for Baloo. The reason for that is because I chose the self-insured route. This means that I put a certain amount per month on a savings account that I could use in case of a medical emergency with Baloo. However, I put about $200/month in that account, which is a lot more than I’d pay for insurance.

When I first got him, I guess I was just lucky that he didn’t have any major incidents. I was definitely a regular vet visit during the first few months he was with me. Once he tore a claw out, once he had a minor ear infection and once I had to go to an emergency vet on Sunday evening because he couldn’t get up anymore and I panicked! Luckily, he only had a tummy ache.

None of these visits left me with bills higher than $300. So, I could always pay them easily from my savings account.

However, it could have come quite differently. It’s not uncommon for puppies to eat something that’s life-threatening and they need to get a surgery costing more than $1’000. Now, imagine you put $35/month in that savings account, instead of paying for an insurance and your puppy has to get surgery after 1 month… Will you be able to pay that from some other fund?

If not, I highly, highly recommend you get an insurance! And even if it’s only for your peace of mind.

I’m sure we all love our pups like family. So, make sure you can also provide them with the medical care they deserve!

If you want to learn more about other options to pay and save on vet bills, make sure to check out my article on how to pay vet bills, even in emergencies and these 9 tips to save money on vet bills.

*Disclosure: This post may contain affiliate links, meaning, I get a commission if you decide to make a purchase through one of my links, at no cost to you.